Contents

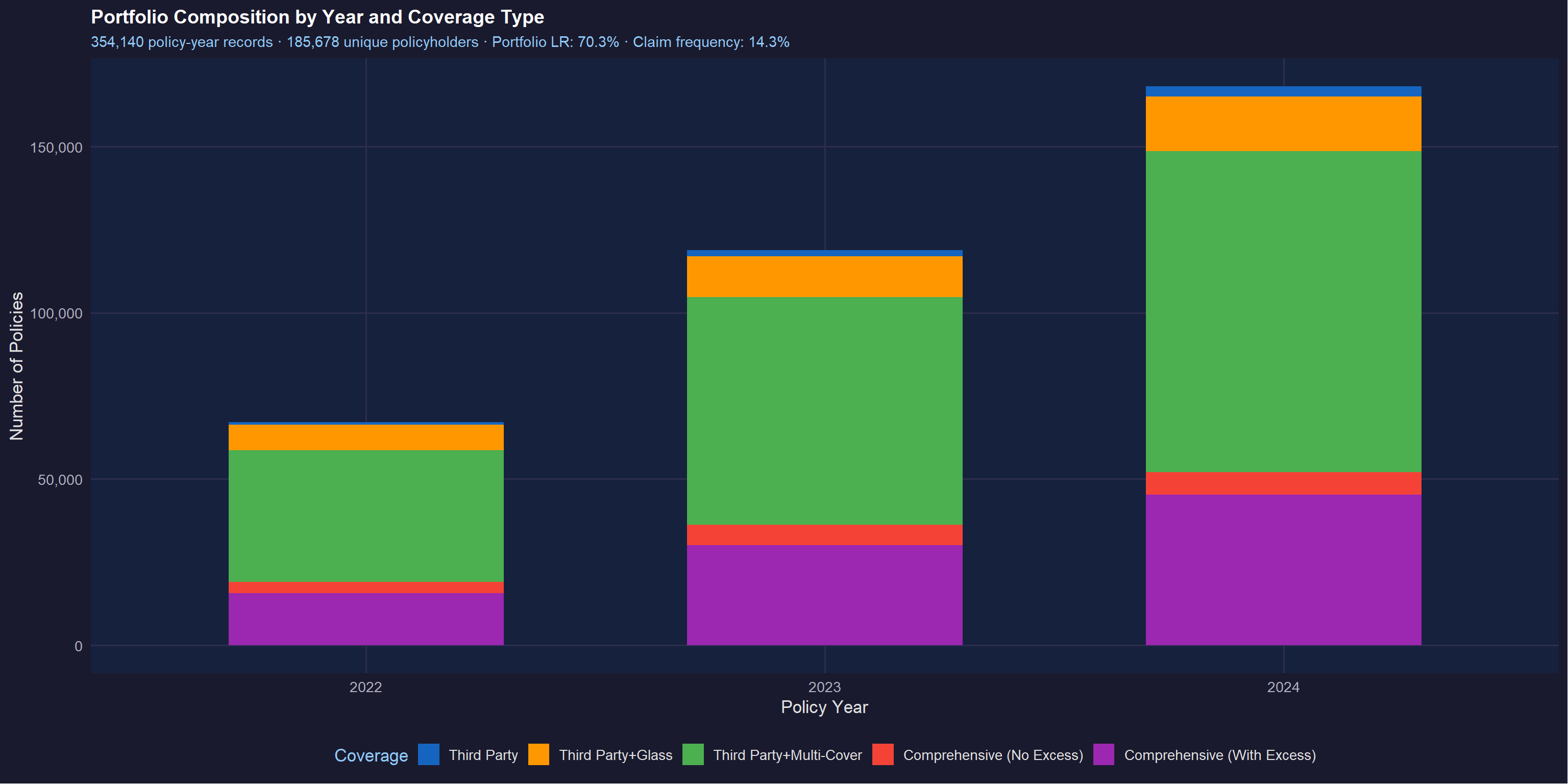

- Dataset Overview — Portfolio scope, structure and key KPIs

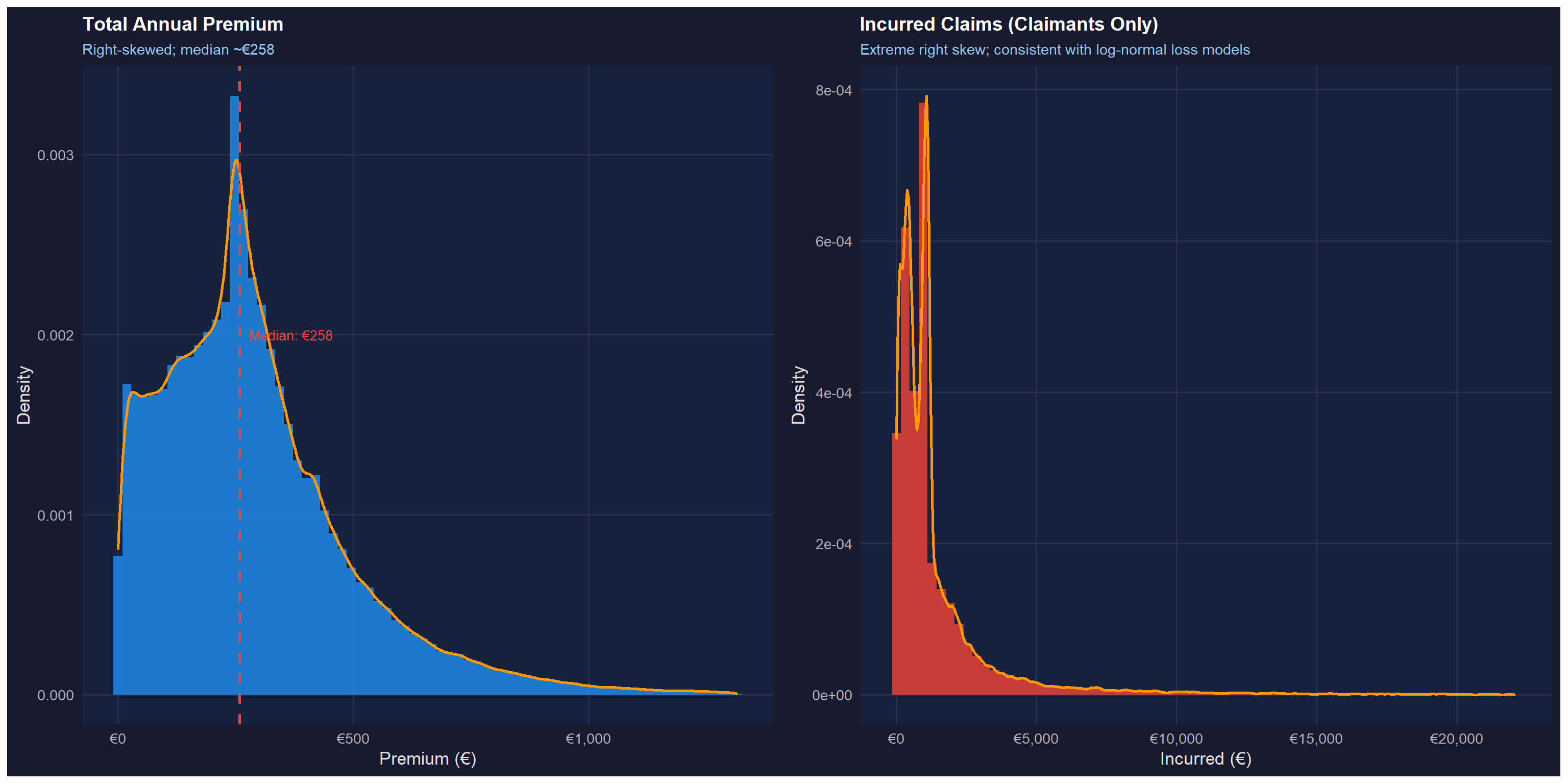

- Univariate: Premium & Claims — Distribution shape and skewness

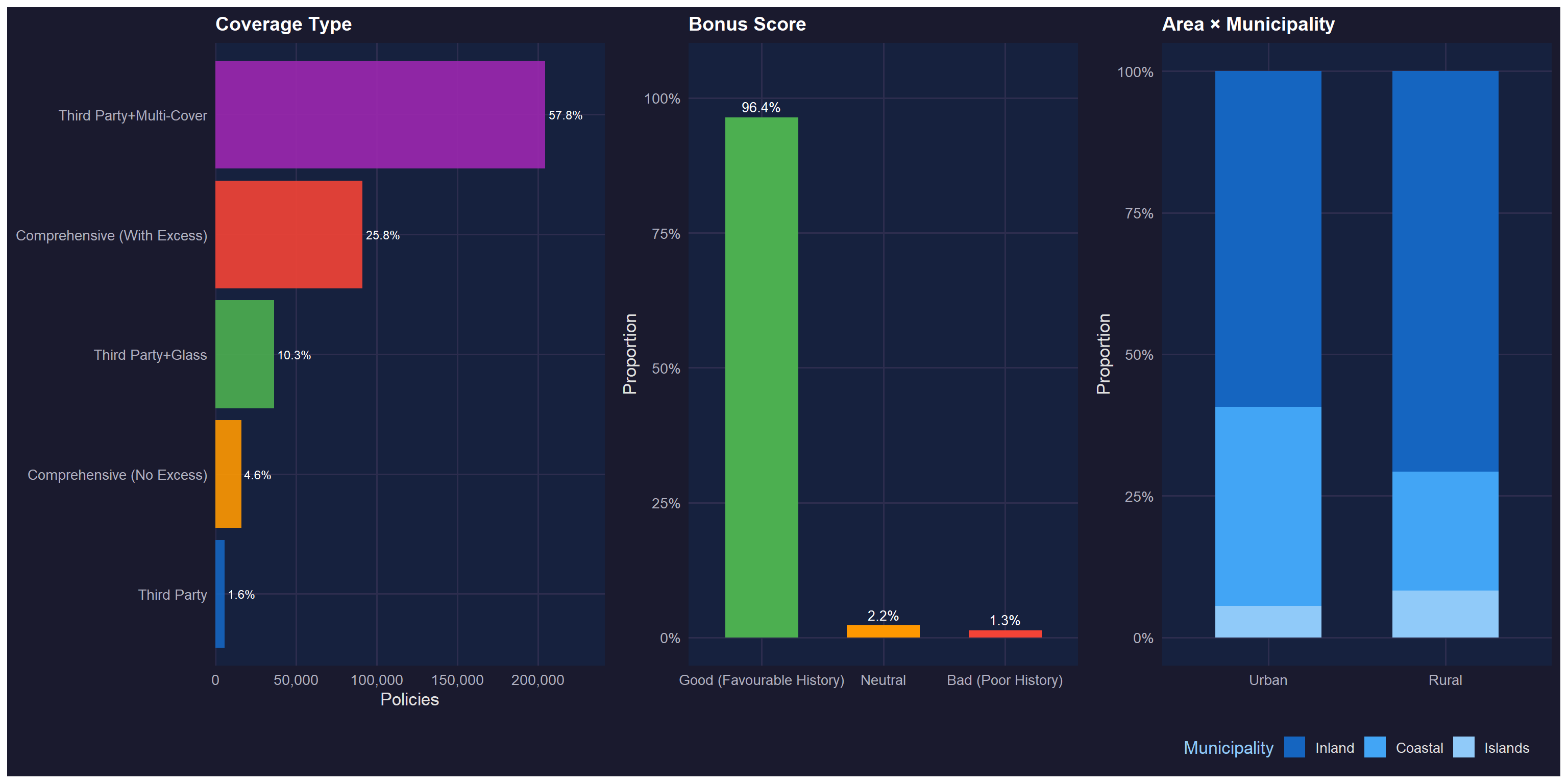

- Univariate: Categorical Variables — Coverage, bonus score and geography

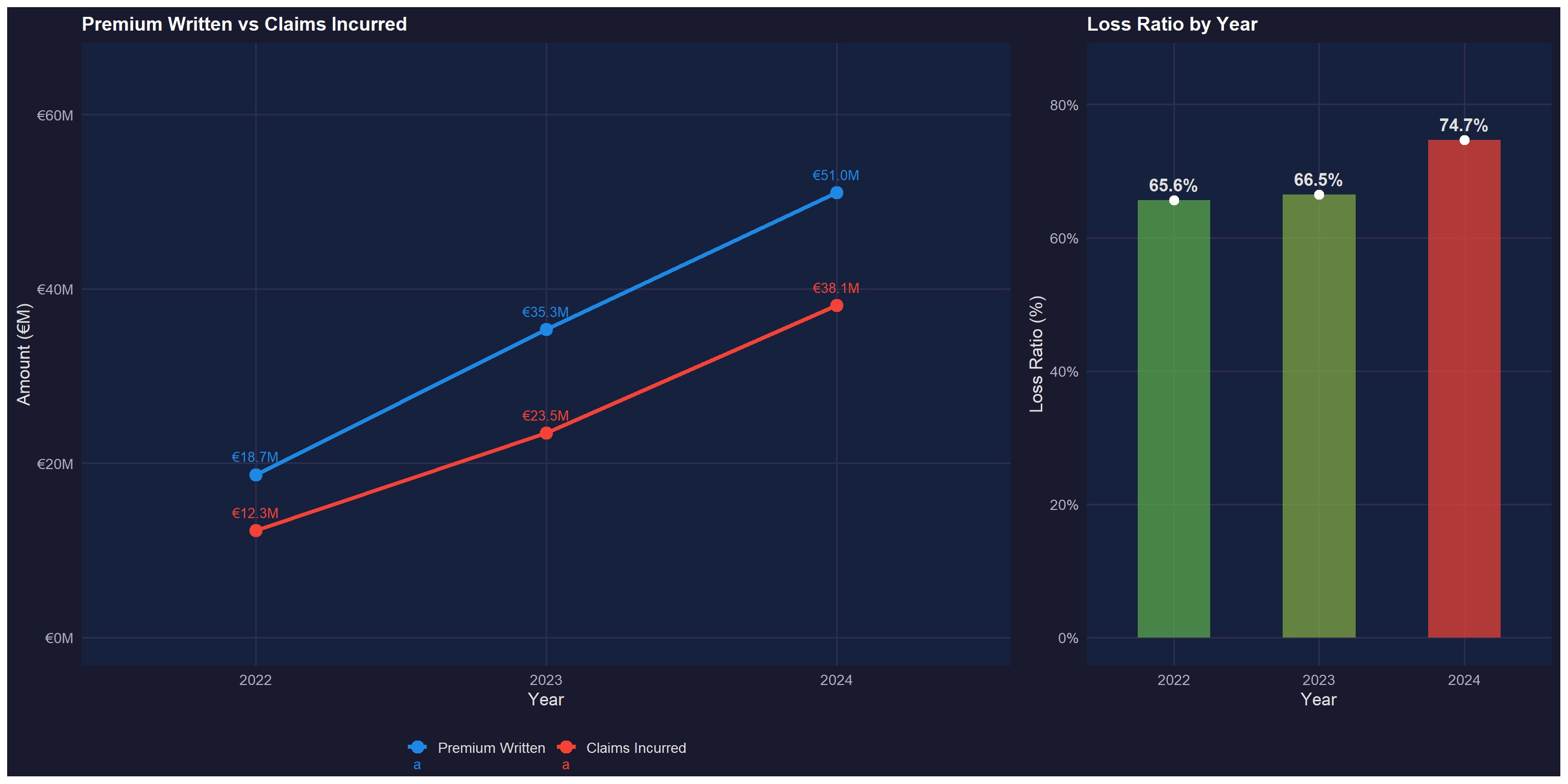

- Temporal Trends — Year-on-year premium, claims and loss ratio evolution

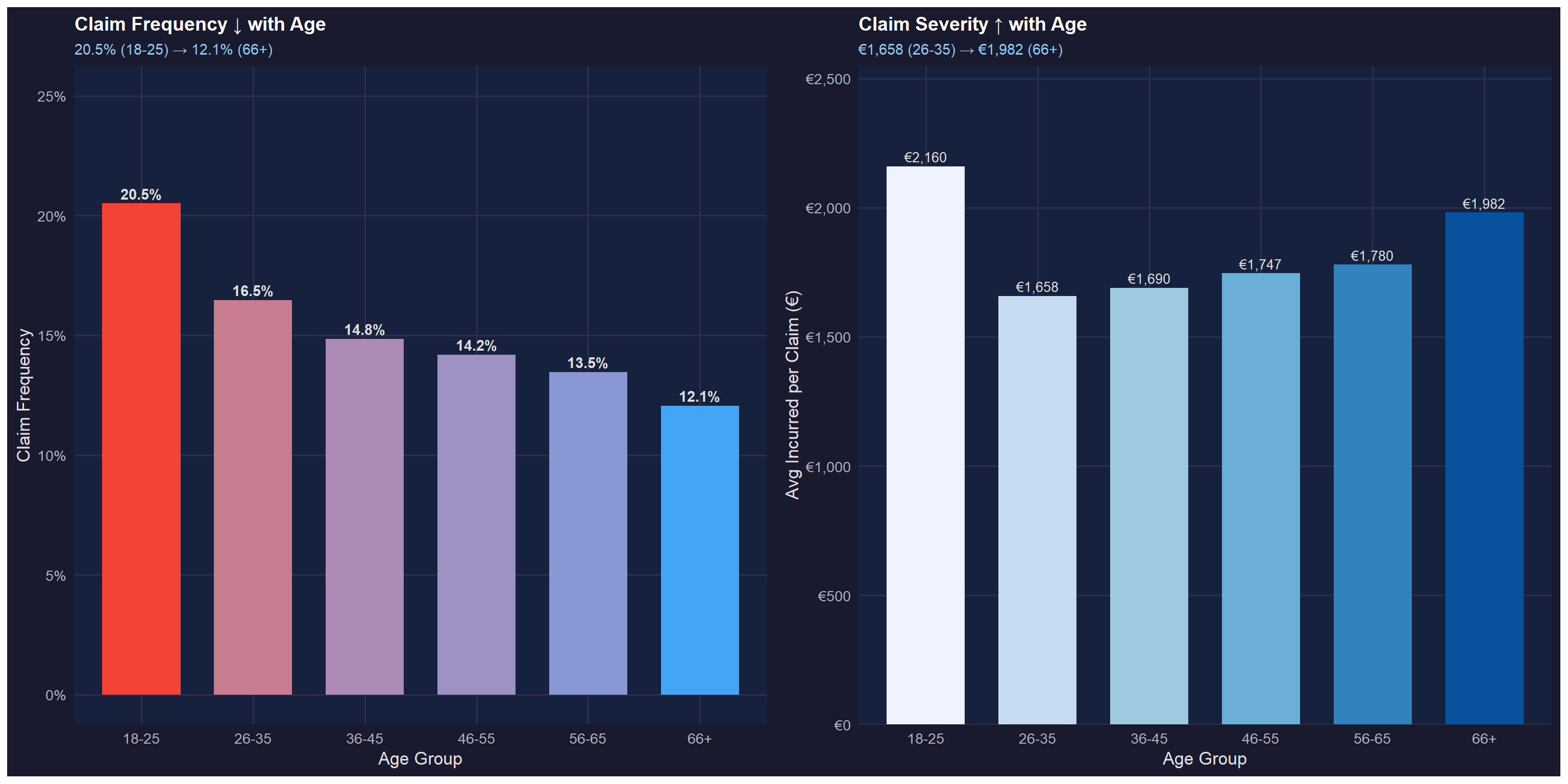

- Bivariate: Driver Age vs Risk — Frequency-severity trade-off

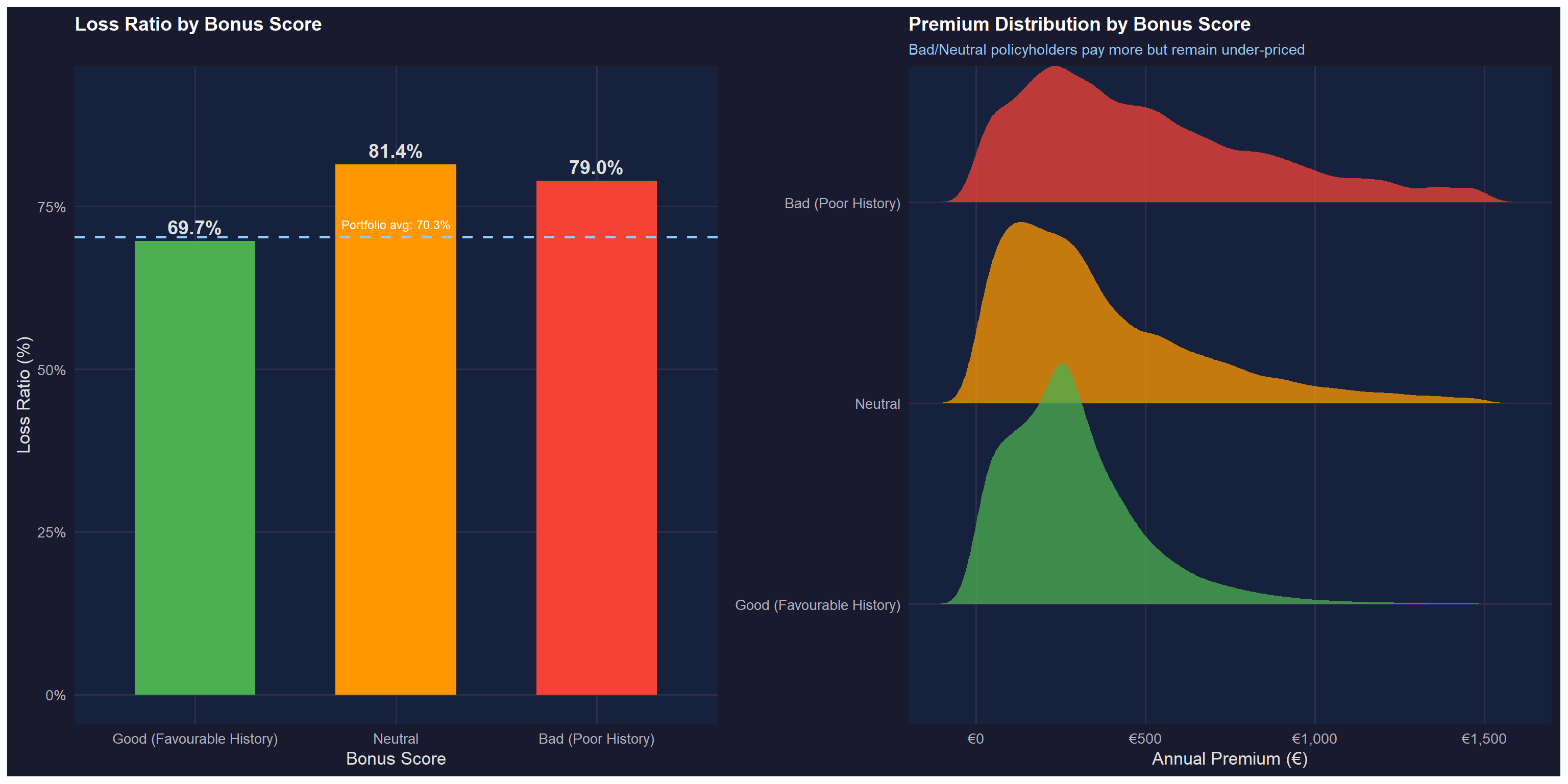

- Bivariate: Bonus Score vs Loss Ratio — Claims history as a risk discriminator

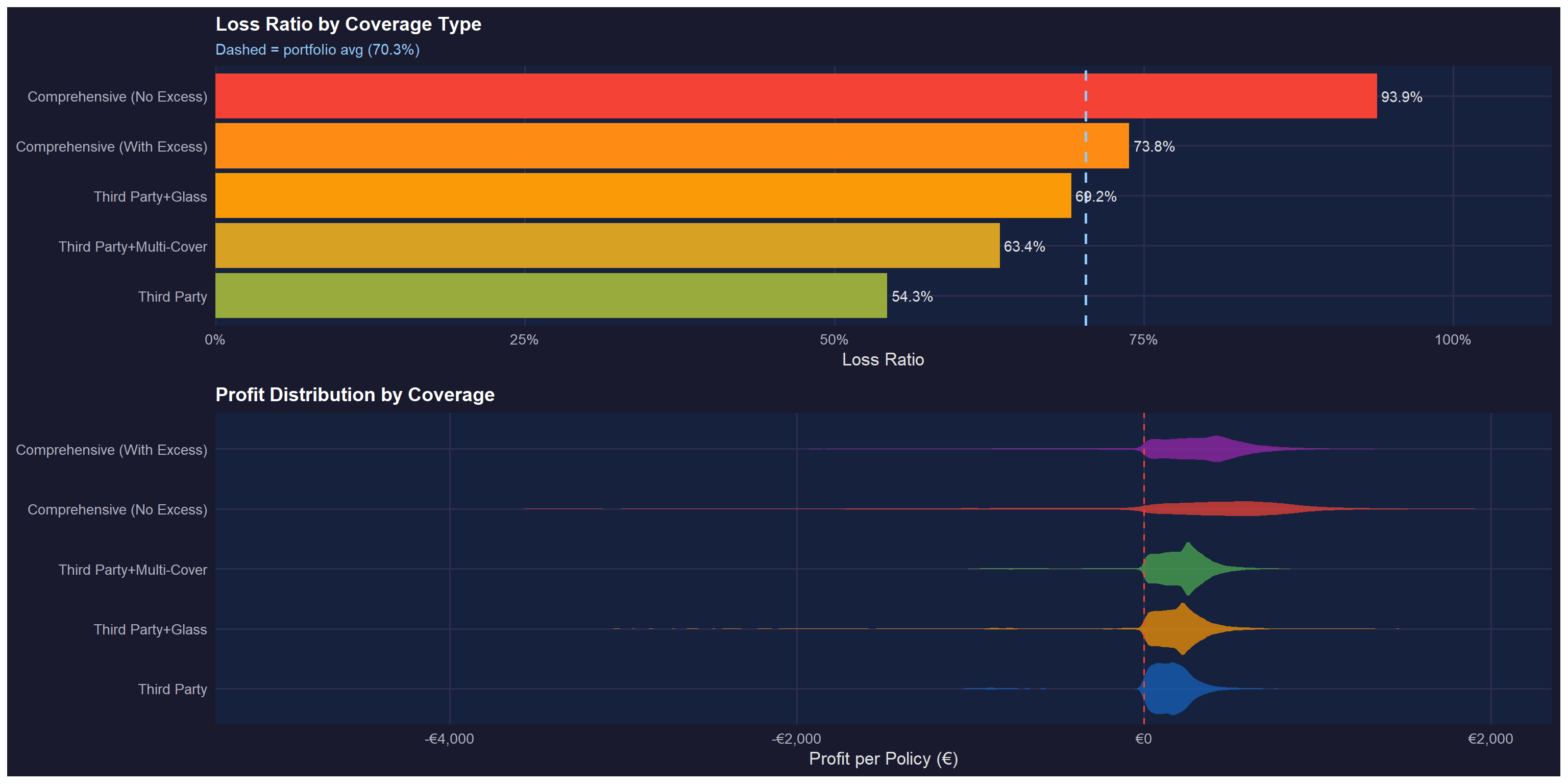

- Bivariate: Coverage Type vs Profitability — Product line analysis

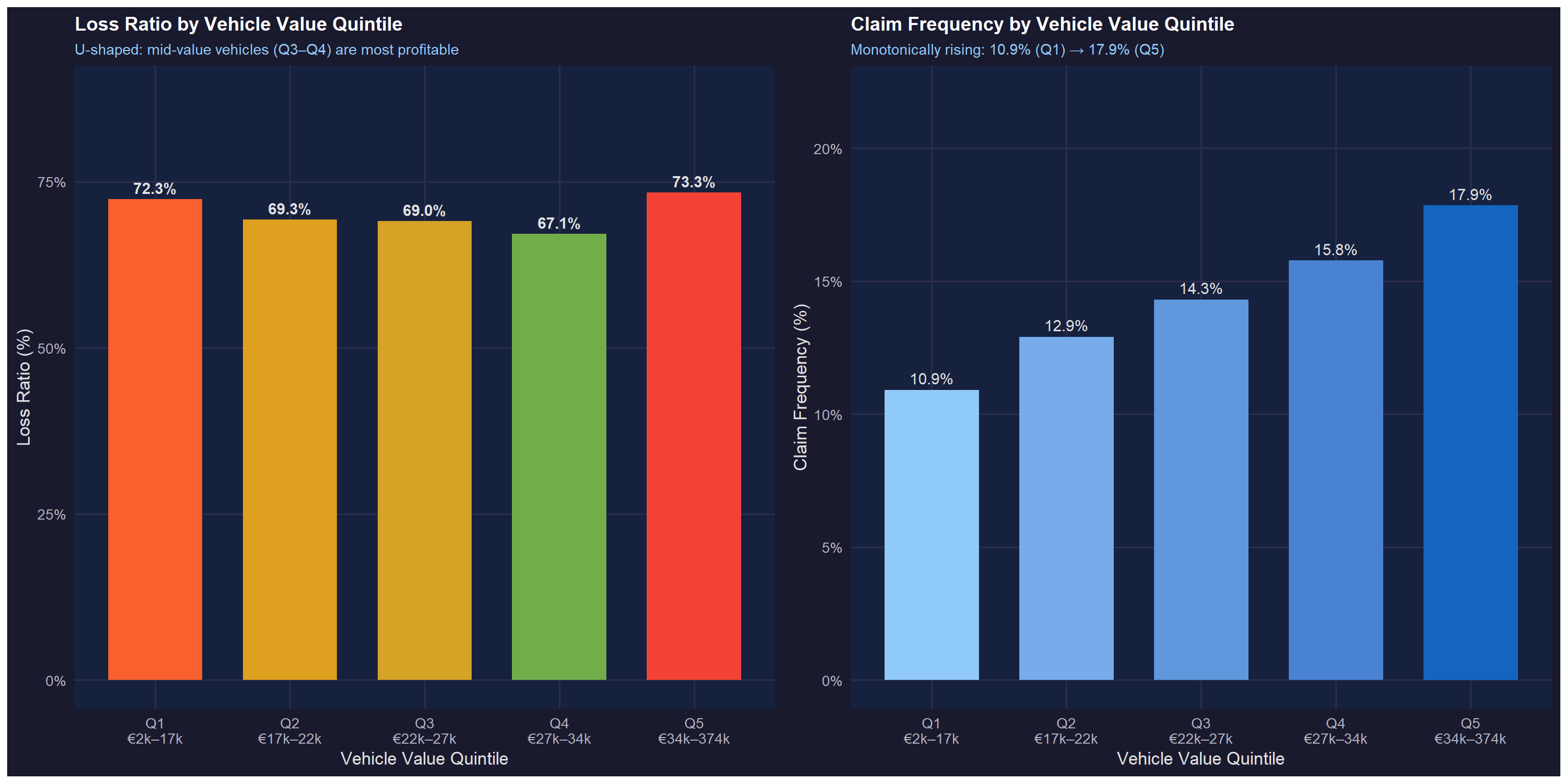

- Bivariate: Vehicle Value — U-shaped loss ratio and rising frequency

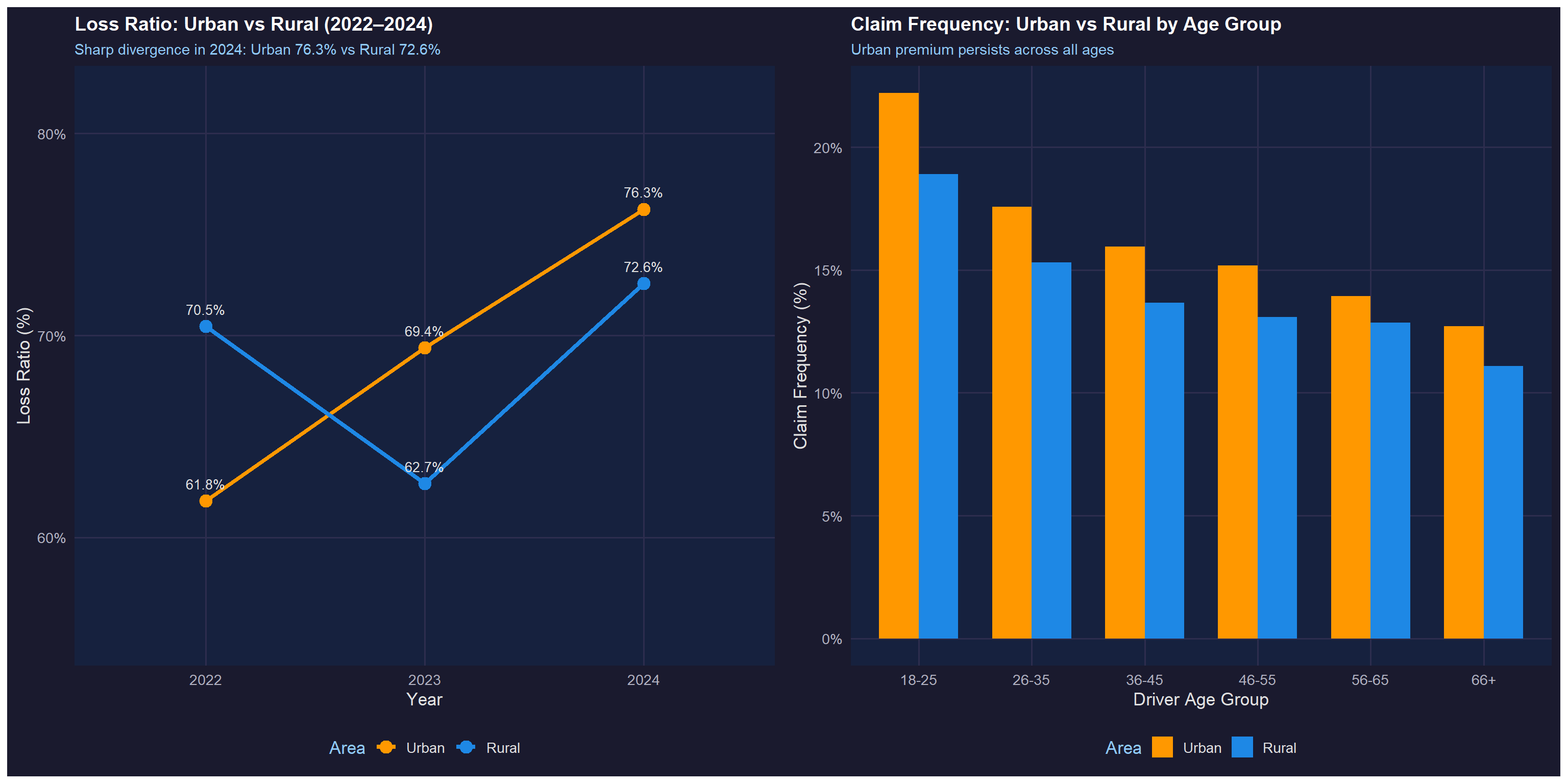

- Bivariate: Urban vs Rural — Geographic risk divergence

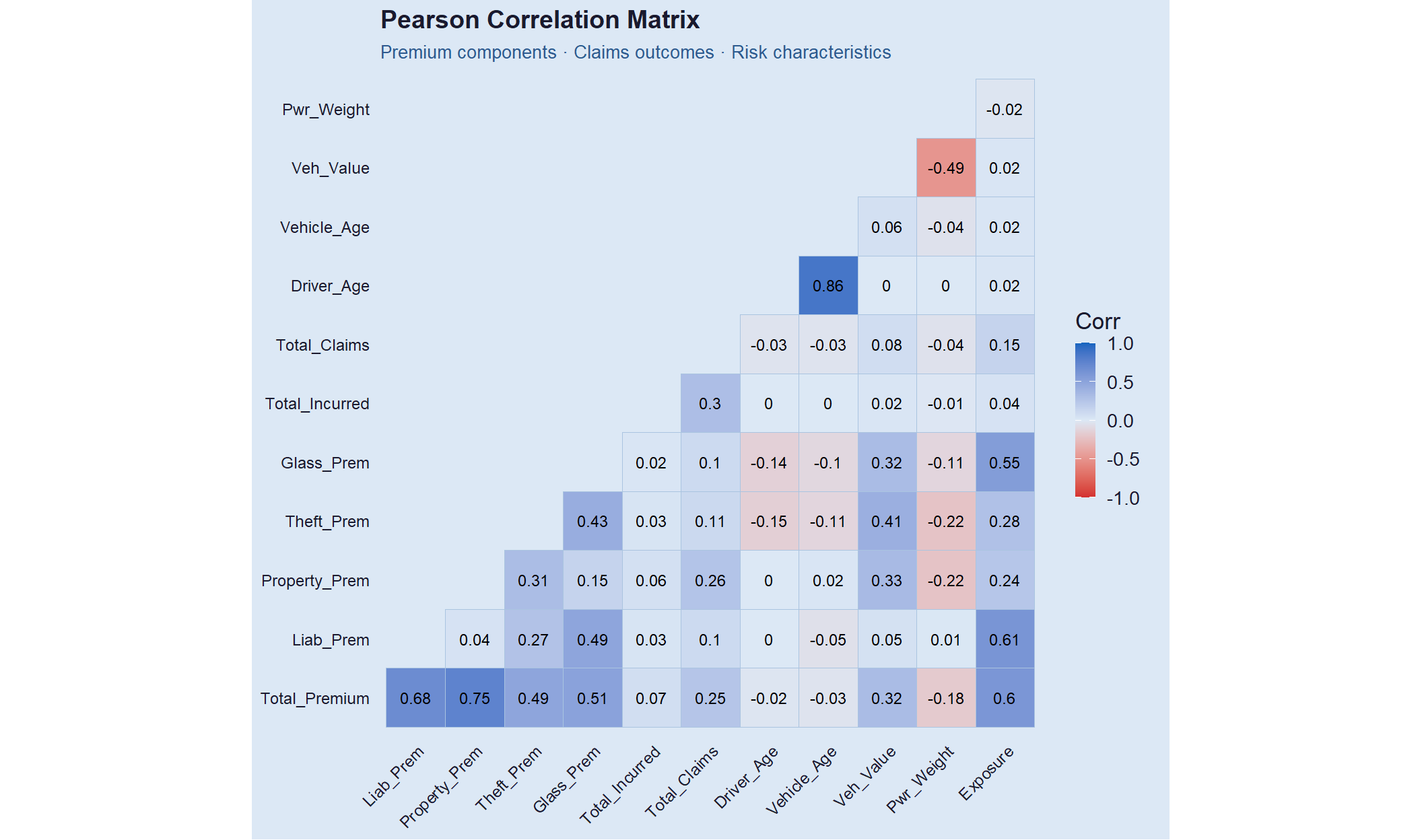

- Correlation Landscape — Premium structure and predictive power

- Key Insights & Recommendations